🔴 The $840 billion delusion of AI disrupting enterprise software

The story making the rounds in tech news media and analyst reports is all about AI eating enterprise software (Salesforce is in trouble, OpenAI is the next Microsoft, B2B adoption is moving at consumer speed, and incumbents are finished). Almost none of this is accurate...

Takeaways:

- The enterprise software moat is structural. High-value, high-regulatory-exposure software (financial reporting, legal, compliance) is immune to AI displacement for at least 7-10 years. The technology is capable, but the liability architecture of large enterprises cannot accommodate probabilistic outputs, regardless of improvements in error rates.

- OpenAI's valuation maths don't work. At $840B on ~$5B ARR, the 160x revenue multiple requires capturing 3× Salesforce's current ARR against entrenched incumbents, while burning $99B cumulatively through 2028 with no visible margin inflection.

- Defense is the only viable exit from the unit economics trap. Only government contracts offer the scale, margin protection, and lock-in that commercial markets structurally cannot. They will turn OpenAI into a defense contractor dependent on government patronage, rather than the civilizational infrastructure layer it is pitched as.

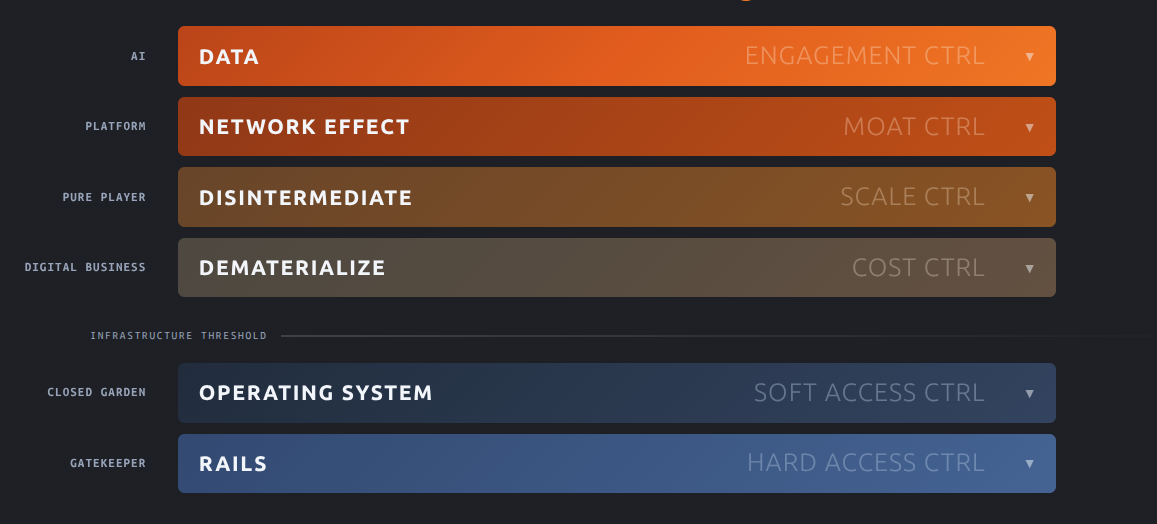

The fracture line nobody draws correctly

The AI-versus-enterprise-software debate is being conducted from afar, as if producing the same code and interface quality were enough to displace Salesforce, SAP, or others. We already had part of this discussion.

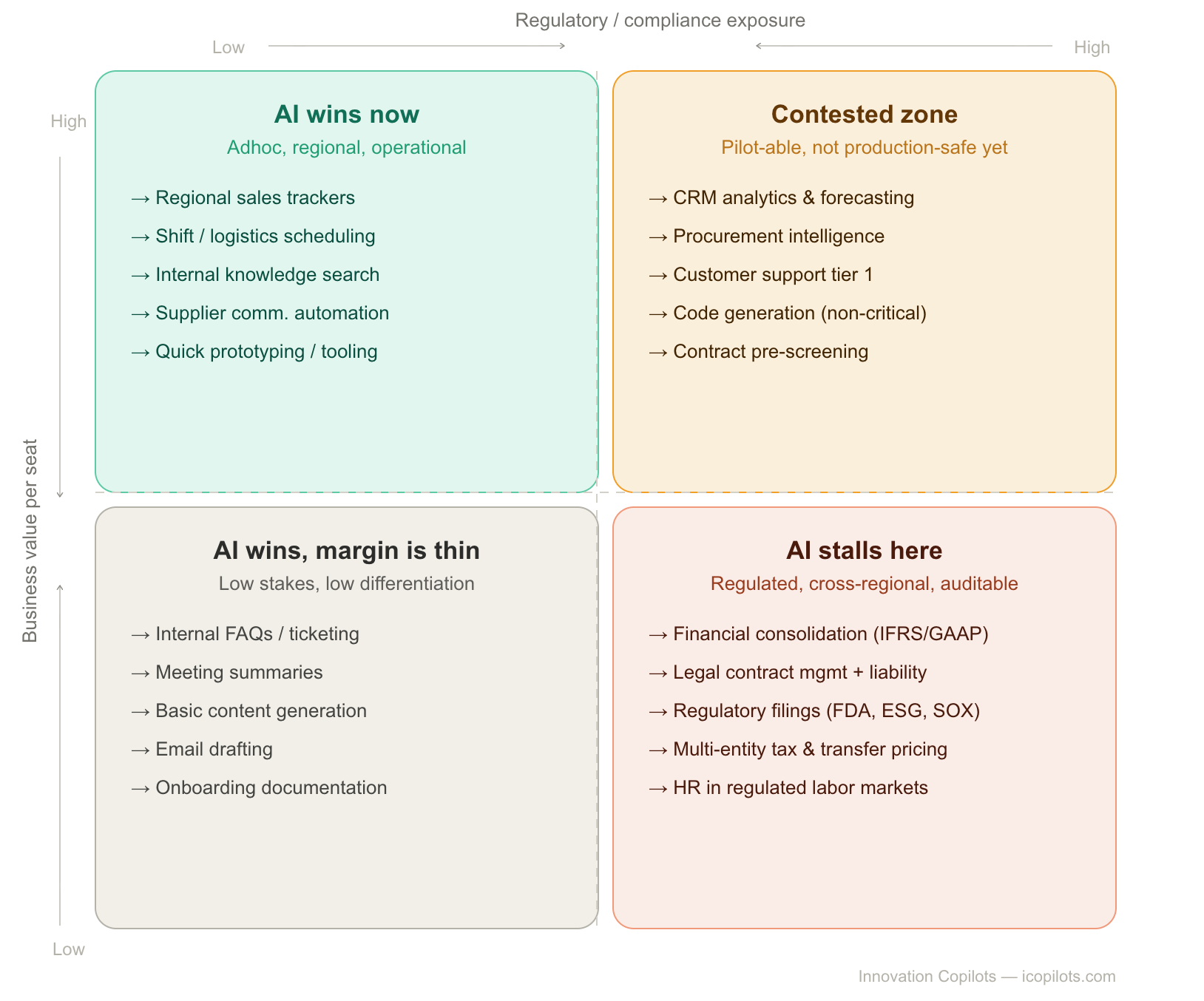

Let me explain further... Enterprise software is not a homogeneous reality, and is certainly not as frail as you could imagine. Parts are structurally protected, and for quite a long time. Here's a quick split of the AI vs. enterprise software reality:

Here, the vertical axis matters as much as the horizontal one.

High business value per seat, combined with high regulatory exposure (the bottom-right quadrant), is where the incumbents are completely safe. It's also where the revenue that would justify a $840 billion valuation actually lives. The top-left is real and accelerating, but it's a low-margin, high-churn market by design. And the two axes together explain why the B2B adoption story being sold to investors is structurally miscalibrated.

Why the hard cases won't crack

The prevailing optimistic view holds that hallucination is an engineering problem and that if you give models another 18 months, the error rate will drop to an acceptable level. This reasoning sounds plausible until you think about what acceptable actually means in a financial restatement context.